The most important insurance cover that MIPS provides is indemnity insurance. Indemnity insurance for healthcare practitioners is also referred to as:

- medical indemnity (typical in Australia)

- professional indemnity (typical in the UK and for other occupations)

- medical malpractice insurance (typical in the USA)

One of the mandatory registration standards of the Medical Board of Australia relates to professional indemnity.

“All medical practitioners who undertake any form of practice must have professional indemnity insurance or some alternative form of indemnity cover… initial registration and annual renewal of registration will require a declaration that the medical practitioner will be covered for all aspects of practice for the whole period of the registration”.

Interns and public hospital employed doctors are frequently members of medical defence organisations (MDOs) or insurers to ensure they have cover for the provision of any healthcare that may fall outside of their work at the hospital (eg gratuitous work) or professional matters where your employer may not be able to represent you (eg coroner court appearance).

On commencement of private practice, practitioners need to ensure that they notify their MDO/insurer to ensure indemnity cover is commensurate with their new risk exposure.

Key terms to understand:

|

Medical indemnity

|

A special type of professional indemnity insurance enshrined in legislation specifically created for health care professionals for the risks arising out of their provision of health care. This covers legal costs and expenses incurred in your defence, as well as any damages or costs that a court may order you to pay.

|

|

Professional issues

|

Can include complaints to employers, health ombudsmen, industry associations, colleges, registration authorities, complaints bodies; complaints by employees and coroners matters.

|

|

Claims made insurance

|

Cover for eligible claims or notifications made in the period of insurance and notified in the period of insurance to your MDO.

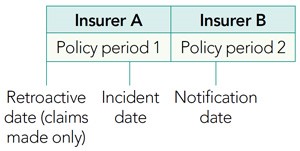

This diagram illustrates a claim under both claims incurred and claims made. MIPS indemnity cover is claims made.

- If the policies were claims-made then the incident would be covered by Insurer B because the incident was first notified in period 2 and occurred after the retroactive date. This is how MIPS' cover works.

- If the policies were claims incurred then the incident would be covered by Insurer A because the incident occurred within the period covered by Insurer A.

|

|

Retroactive cover date

(tail cover)

|

Cover is provided after the retroactive cover date for claims (of which there is no current knowledge) that arise from health care services provided in previous years. It is important to note that most claims are made by patients in the years following the year in which they received the health service triggering the claim.

|

|

Employer indemnified

|

In general terms an employer such as a hospital, is vicariously liable for negligent acts or omissions by an employee in the course of their employment. The obligation of the employer may not extend to ‘professional issues’ relating to their employee. If you work in a hospital and undertake no, or limited private practice, then you can acquire ‘100% employer indemnified’ insurance so that you pay a lower membership fee/premium than if you were fully doing private practice. This accounts for the fact that your employer is providing you with indemnity cover.

|

|

Duty of disclosure

|

There is a common law legal duty before entering a policy of insurance (for the first time and at any renewal, extension, variation or reinstatement of the policy) to disclose anything that you know, or could reasonably be expected to know, that is relevant to the decision to insure you and the terms and conditions on which you are insured. For example, any previous claims and or investigation history and/or previously unreported incidents. If you fail to comply with your duty of disclosure your rights under a policy may be jeopardised.

|